Kiwi Housing Trends Report 2.0

How rising costs are reshaping the New Zealand dream

New data from OneChoice reveals a growing disconnect between aspiration and reality for young New Zealanders navigating the housing market. While the desire to own a home remains strong, rising living costs, affordability pressures, and shifting expectations are forcing many to rethink what the ‘New Zealand dream’ looks like in 2026.

Based on research conducted with over 500 New Zealanders, the OneChoice Kiwi Housing Trends Report 2.0 highlights a generation adapting to financial constraints, longer timelines, and increasing reliance on family support.

Key findings

- Around 2 in 3 (66%) expect living affordability to worsen over the next decade

- Over 1 in 2 (54%) now define the ‘New Zealand dream’ as financial independence, ahead of home ownership

- Close to 1 in 2 (48%) of first-home buyers expect support from the ‘Bank of Mum and Dad’

- Nearly 9 in 10 (88%) still see home ownership as a core life goal

- Exactly 9 in 10 (90%) renters believe rent is overpriced

The New Zealand dream is evolving

For decades, home ownership has been seen as the ultimate marker of success. But today, that definition is shifting.

Over 1 in 2 (54%) now define the ‘New Zealand dream’ as being financially independent, ahead of owning a home (44%). At the same time, nearly 2 in 3 (65%) believe the traditional dream of home ownership is no longer relevant.

Despite this shift, the aspiration hasn’t disappeared. Nearly 9 in 10 (88%) still believe buying a home is a core life goal. However, around 4 in 5 (80%) say it is unaffordable today, and more than 4 in 5 (84%) feel younger generations are being locked out of the market.

Looking ahead, around 2 in 3 (66%) expect living affordability to worsen over the next decade, reinforcing a growing sense of uncertainty about the future.

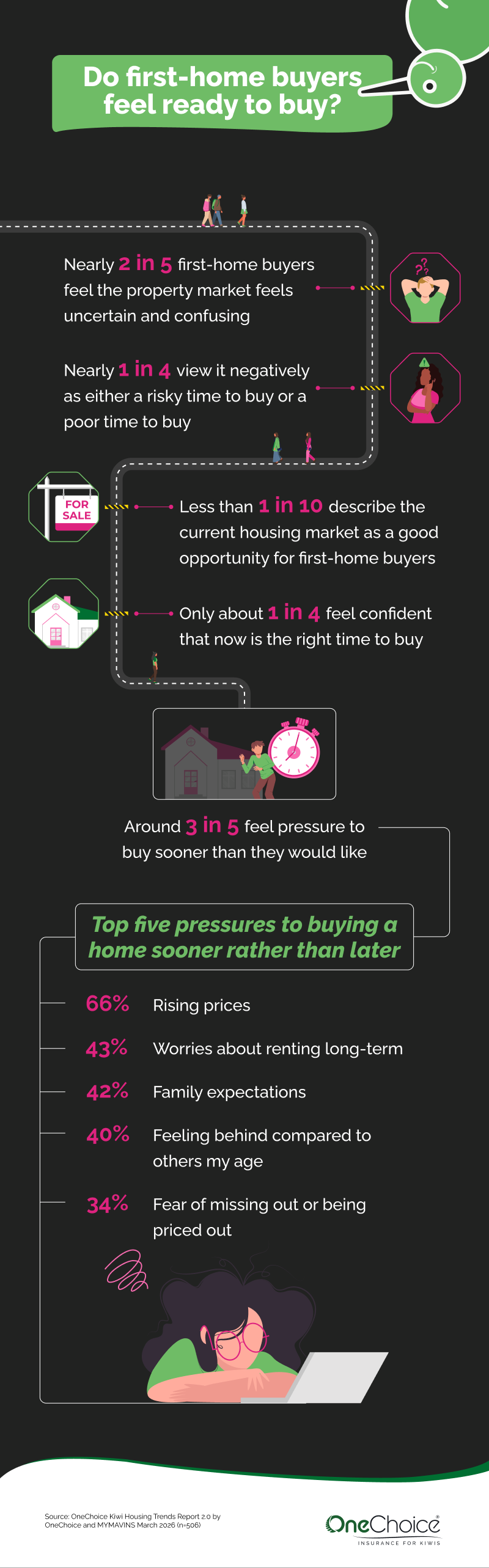

The first-home buyer paradox

Pressure to buy vs confidence to act

Today’s first-home buyers are caught in a clear contradiction – strong pressure to buy, paired with low confidence in the market.

Around 3 in 5 (61%) feel pressured to purchase sooner rather than later, yet over 7 in 10 (71%) lack confidence that now is the right time.

What’s holding buyers back

This hesitation is driven by a combination of financial and emotional pressures:

- 3 in 5 (61%) worry about saving a sufficient deposit

- Over half (58%) fear prices will rise before they can buy

- Half (50%) are concerned about job or income security

Longer timelines to home ownership

These pressures are pushing timelines out significantly. Nearly 4 in 5 (78%) expect to wait at least three years before buying, with the proportion expecting to wait more than 10 years doubling from 10% in 2022 to 20% in 2025.

Caught in the rent trap

Rent is consuming more income

For many, renting is no longer a stepping stone – it is a barrier.

Exactly 9 in 10 (90%) renters believe rent is overpriced, and around 1 in 3 (33%) spend at least half their income on rent. A further 38% spend between 30% and 49%.

Cutting back on essentials

This financial strain is having a ripple effect across everyday life:

- Nearly 4 in 5 (78%) are cutting back on essentials such as groceries, healthcare, and transport

- Around 3 in 4 (76%) feel ‘trapped’ as renters, unable to save for a deposit

- Nearly 9 in 10 (89%) are worried about their ability to afford a home

The emotional toll of renting

Beyond finances, the emotional toll is also significant. Among renters experiencing rent increases, nearly 4 in 5 (78%) say it has impacted their overall wellbeing.

The ‘Bank of Mum and Dad’ under pressure

Family support is becoming essential

With affordability challenges mounting, family support has become increasingly important.

Close to 1 in 2 (48%) first-home buyers expect financial assistance from family, most commonly to help with a deposit.

The risks of relying on family

However, this reliance comes with consequences:

- 7 in 10 (70%) say losing family support would delay their ability to buy

- Nearly 2 in 5 (38%) say it would set them back for many years

- 7 in 10 (70%) are concerned about the financial pressure placed on parents and grandparents

New-build concerns are eroding trust

Growing fears around quality

Confidence in new housing developments is also declining, adding another layer of complexity to the market.

Nearly 2 in 3 (66%) are worried about the quality of new builds, and over half (53%) have either experienced issues themselves or know someone who has.

Impact on buyer behaviour

These concerns are influencing buyer behaviour:

- More than 1 in 2 (57%) are less likely to consider a new build

- Over 7 in 10 (72%) believe homes are being constructed too quickly

- Around 2 in 3 (67%) find it harder to trust compliance and safety standards

Calls for greater accountability

There is also a strong call for accountability, with 88% believing developers should be held more responsible for long-term build quality.

A generation adapting to a new reality

Delaying major life decisions

The findings paint a picture of a generation recalibrating expectations.

Around 7 in 10 (71%) are delaying major milestones – from starting a family to changing careers – due to housing pressures, with more than 4 in 5 (84%) saying these costs are impacting their ability to pursue life goals.

Redefining success beyond home ownership

Home ownership remains a goal, but it is increasingly being delayed, downsized, or supported by family. At the same time, financial independence is emerging as a more attainable and realistic benchmark of success.

What this means for New Zealanders

The study provides a clear snapshot of a housing market under strain. For many, the path to home ownership is becoming longer and more uncertain. In response, New Zealanders are redefining success, adjusting expectations, and finding new ways to navigate an increasingly complex financial landscape.

Methodology

The OneChoice Kiwi Housing Trends Report 2.0 is based on independent research commissioned by OneChoice and conducted by MYMAVINS between 15 and 29 December 2025.

The study surveyed 506 New Zealanders aged 18 to 39 via an online quantitative survey. The sample is representative of the New Zealand population by age, gender, region, and income.

Comparisons to 2022 data are based on a previous study of respondents aged up to 42, with differences noted where relevant.

7 May 2026